The Problem With Most Venture Studios (And Most VC)

Traditional venture capital is built on the Power Law. By investing in dozens of companies and hoping for a single home run, the model inadvertently fosters low-touch relationships, misaligned incentives, and a “spray-and-pray” approach that has led to a 90% pre-Series A failure rate.

Venture studios were meant to address these issues. The idea was sound: give founders capital, talent, and infrastructure from day one and raise the odds of success. Yet the majority of studios have earned a reputation for being misaligned, undercapitalized, founder-unfriendly, or simply rebranded incubators.

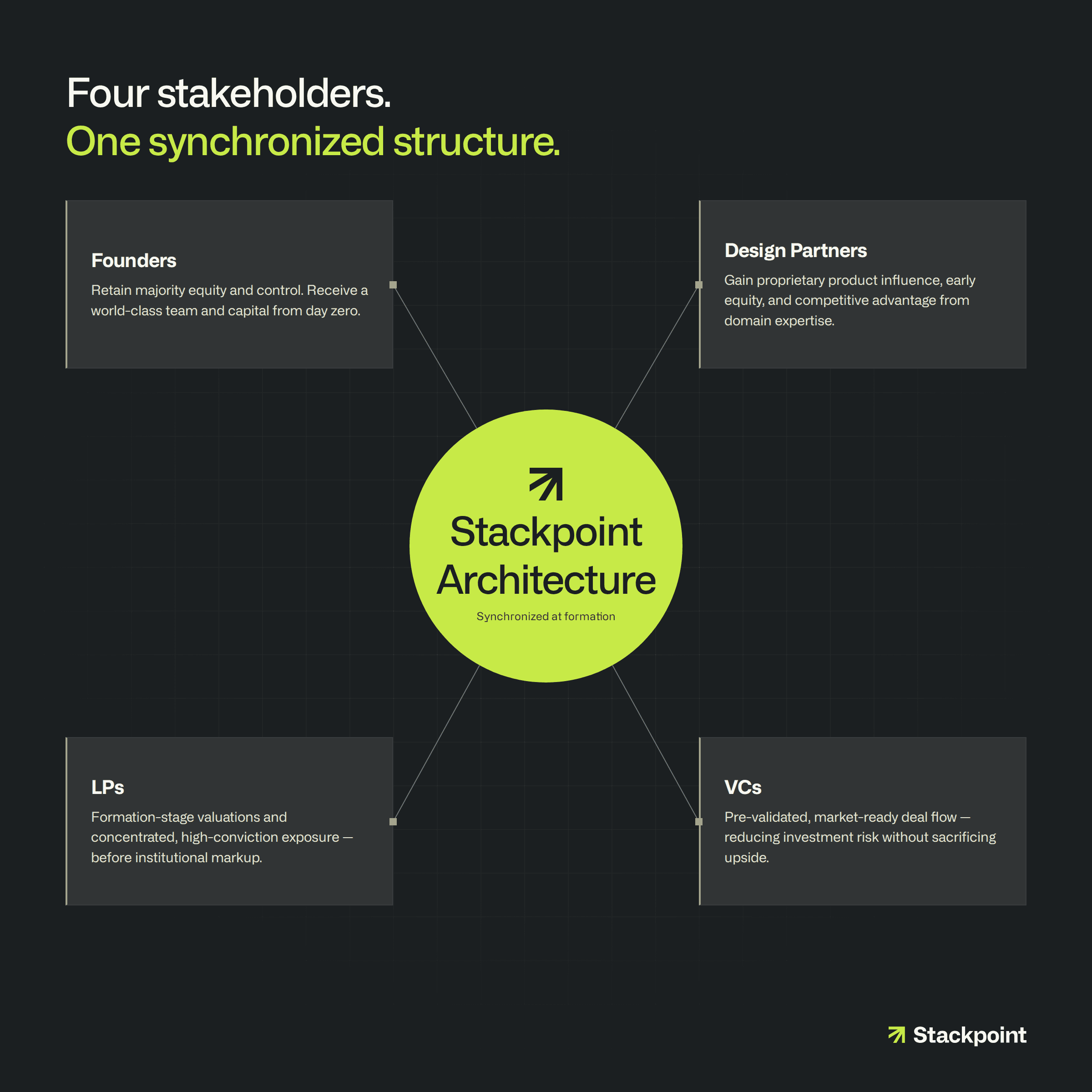

Stackpoint was built to be the exception. Here is how our structure creates value for every stakeholder in the ecosystem: founders, design partners, LPs, and the VCs who fund our companies.

The Studio Model's Design Problem

The venture studio model emerged to solve a real problem: most startups fail long before they ever have a chance to become great businesses. By providing founders with capital, talent, and infrastructure from day one, studios promised to increase the odds of success. The model was also attractive for investors - greater ownership in high growth startups with a higher success rate would give the upside of traditional venture capital while mitigating some of the risk.

But the category has struggled to reach its potential. A handful of studios have produced impressive outcomes (companies like Snowflake, Hims, Affirm and Dollar Shave Club all trace back to studio models), yet the category as a whole still faces persistent questions about founder alignment, unit economics, and scalability.

Many studios face a series of structural tensions:

How much equity can a studio take while still attracting exceptional founders?

Can a studio provide meaningful operational support without creating conflicts with founders and investors through consulting fees and charge-backs?

Can a studio develop deep expertise in a market to provide compounding value to design partners and founders, or does it become spread too thin across industries and business models?

How do you create companies systematically with real market demand rather than products searching for customers?

These tensions surface even across studios run by highly experienced operators. They’re the natural consequences of misalignments baked into many Studio structures.

So at Stackpoint, we started from a different question: what would a venture studio look like if every stakeholder's incentives were aligned from day one?

The result is an architecture built around four constituencies: founders, design partners, LPs, and venture investors. Each group's success reinforces the others.

1. Founders: More Leverage, More Ownership

Stackpoint sets a high bar for the founders we partner with. We back serial entrepreneurs who have built teams, shipped products, and raised capital before.

You might think great founders like these can bootstrap, raise traditional venture capital, or recruit their own co-founders, so why would they need a venture studio? Stackpoint is set up to make the partnership the obvious choice, by building a value proposition compelling enough to beat every one of those alternatives. For a repeat founder, the real question is simply which path gets there fastest and with the best odds of success. We designed Stackpoint around that calculus.

Founders retain majority equity. Our structure ensures that founders maintain the majority of equity, long-term upside, and control—always. According to Carta’s 2026 Founder Ownership Report, the founding team of the median digital startup retains 37.5% of total equity after raising a Series A. Stackpoint founders typically end up with more, and they reach Series A about 3x more often than a typical VC-backed startup. Governance follows the same principle: founders run the board and make the decisions, with Stackpoint as a partner rather than a controlling shareholder. Our role is to amplify great founders, not replace them.

A world-class team from day zero. Most founders spend 12–24 months recruiting their first engineering, product, design, and go-to-market talent—and many of those hires fail. We provide a dedicated team from the outset, offering a level of talent typically inaccessible to early-stage startups, supported by in-house experts to help hire their next critical employees.

“The economics are often better than the traditional co-founder route post-Series A — and you start with a team that took others years to build.”

De-risking problem-market fit and product-market fit. Before a company is even formed, Stackpoint assembles strategic design partners who provide proprietary data, workflow access, domain expertise, and direct feedback. Our discovery process puts that access to work through journey mapping, on-site user shadowing, and concept testing, so we can confirm we're solving a real problem with the right solution before significant capital goes in. Just as important, these relationships become the company's early distribution: design partners often turn into first customers, which accelerates adoption from day one. Founders know how hard customer access is to earn. With Stackpoint, it's built into every company from the start.

Programmatic capitalization. We eliminate the distraction of early-stage fundraising. With $1M committed at formation and $5M reserved for Seed and Series A, founders can focus entirely on building and hitting their milestones, knowing the capital will be there.

Zero charge-backs. Some studios erode founder equity by billing portfolio companies for design or engineering sprints. Stackpoint contributes all of its resources as sweat equity, so our incentives stay aligned with the founder's: we only make money when the company succeeds.

Built for repeat entrepreneurs. We partner with serial founders who have built and led teams and products, raised capital, and navigated complex markets. Many have had co-founders in the past. They know what it takes to succeed and they want the highest ROI for their time. Rather than trying to find a single co-founder who can complement their skills in all areas, they get an entire team, capital, and ecosystem on day one. The result is a high-execution, peer-to-peer relationship from the start.

A "try before you buy" period. A 4-to-6-week discovery phase lets founders work with our team before anyone commits, so both sides can validate the partnership before forming the company.

2. Design Partners: Co-Creators and Co-Investors

Industry incumbents have become accustomed to technology products overpromising and underdelivering. Most sell at them, arriving with a product already architected and a valuation too high to justify an investment, instead of listening to their problems and building with them. Many incumbents choose to wait: let someone else fund the R&D, then buy the product once it works. This waiting period is expensive: incumbents can lose their competitive advantage, and they forfeit the chance to shape the product and own a piece of it on the way up. The data, domain expertise, and workflows they've refined over decades have real, independent value—and the operators who put those assets to work early capture upside that the ones who wait give up.

On the other side of the equation, AI startups need exactly what these companies have: validated problems, proprietary data, and willing customers to test and deploy at scale. It's a win-win when the two work together, and Stackpoint's model is built to serve both the incumbent's and the portfolio company's needs.

What the win-win looks like:

For design partners, they get:

Product influence. Direct input into the roadmap, so the product gets built around how they actually operate rather than a generic version of the problem.

Financial skin in the game. Design partner CEOs typically have an opportunity to invest early. In exchange for early access and proprietary data, they get to buy equity when it's cheapest, owning more than they would as an LP in a typical VC and sharing in the upside with the product's success.

Preferred pricing. Free use of the product during the beta, and a discount once it's commercially available.

Seamless collaboration. We've run this process many times. Partners get fast insights, airtight data security, and minimal disruption to their day-to-day.

For portfolio companies, they get:

Targeted consortiums. Before we launch any company, we assemble a minimum of 3 to 5 design partners: mid-sized, agile companies with $1M+ revenue potential that share a specific pain point. These are meaningful potential customers.

Proprietary data moats. Access to non-public enterprise data and on-site workflows lets us build defensibility into each company from day one. This is the kind of workflow-deep, data-driven moat that holds up even in an AI bubble, because it compounds with use and is hard for any outside competitor to replicate.

Validated demand. We don't build on hypotheses. Users become design partners, strategic investors, and eventually first customers. By launch, the company already has a line of paying clients.

This is exactly how the model played out with Dirt, an AI-native land development platform Stackpoint co-founded. Barron Collier Companies brought decades of operating knowledge in land feasibility, entitlements, and cost modeling, helping shape the product around real-world development workflows rather than abstract assumptions. For design partners, the value was not just early access; it was the chance to influence a product built for their actual operating needs, invest early, receive preferred pricing, and capture upside if the company succeeds. We covered the Barron Collier example in more detail in our deeper case study on how private companies can turn operating expertise into venture-scale assets.

That value proposition is resonating: demand to partner ran so high that Dirt had to cap its design partner program at seven companies, turning away eight of the 15 that wanted in.

3. LPs: Concentrated Exposure and Compounding Alignment

Our LP base is a strategic engine, providing far more than just capital.

Concentrated exposure. We offer a home for LPs frustrated by traditional VC. Instead of a diluted bet across dozens of unknowns, they get concentrated, high-conviction exposure to a focused portfolio of vertical AI companies. Because of the structural advantage of the studio model, that also means roughly 5x more ownership per dollar at initial investment than a traditional VC.

Compounding alignment via co-investment. LPs receive pro-rata co-investment rights at reduced fees, generating an estimated 70–75 cents of co-investment for every dollar committed to the fund.

Multiple paths to liquidity. Large ownership stakes allow for strategic acquisitions and secondary sales, reducing dependence on "unicorn-or-bust" outcomes. A single modest acquisition can return an entire fund. A unicorn outcome results in returns well beyond traditional VC.

Strategic AI exposure at formation-stage valuations. While traditional investors are forced to choose between public market premiums and late-stage rounds with inflated multiples, Stackpoint provides a high-conviction alternative. We offer direct ownership in vertical AI companies at formation, bypassing the institutional markup. Our LPs capture the highest upside by entering before the market froth, securing positions at rational entry points.

4. VCs: A Symbiotic Partnership

While most studios compete with VCs, Stackpoint has built a symbiotic, collaborative ecosystem.

VCs as deal flow partners. Because we build from scratch, VCs bring us opportunities where they have a strong thesis but no company or team to execute it. We create an investable company; they provide the scale capital. We've run exactly this play on companies such as Whale and Truelist.

Market-validated pricing. We never price our own portfolio. External VCs always set the valuation, eliminating signaling risk and conflicts of interest and ensuring all reports are market-validated. A VC partner leads, but we continue to invest capital.

Asymmetric intelligence. By the time a VC leads a round, we have 6–12 months of operating data, live user feedback, and customer validation, providing an intelligence advantage no outside investor can match.

5. The Proof in the Numbers

Across Fund I:

80%+ of Stackpoint companies raise meaningful outside capital, 3x higher than typical startup fundraising benchmarks, based on Startup Genome research and Carta’s Q1 2024 VC fund performance data.

Fund I tracking top 5% of 2021 VC vintage in terms of TVPI according to Cambridge Associates.

$400M+ equity value created and $90M+ in capital raised across the Stackpoint portfolio in under 5 years through a difficult funding environment.

One of ~10 US venture studio platforms to raise $100M+.

The Structural Advantage: Universal Alignment From Day One

Most venture models optimize for one stakeholder at the expense of the others. Founders get diluted, design partners get treated as free user research, and LPs get small stakes and long liquidity cycles. Each model works for whoever sits at its center, and shortchanges the rest.

Stackpoint's advantage is that alignment is built into the structure rather than promised on top of it. Founders keep majority equity and control. Design partners help shape the product and buy equity at its lowest price. LPs get concentrated exposure and multiple paths to liquidity rather than a diluted, unicorn-or-bust bet. VCs get pre-validated companies to lead and price. Each stakeholder's success makes the others more likely, and that compounding only works because the incentives are aligned from day one.