Seed Is the New Series A

AI has rewritten the math of company building. Startups that once required years of development and millions in funding are now reaching scale with leaner teams and far less capital.

AI-native companies are achieving revenue milestones that previously demanded large headcounts and significant burn. The median AI-native startup now reaches $100M ARR faster with just 225 employees—compared to 785 for legacy SaaS companies (Bessemer, Lean AI Leaderboard). This isn’t a marginal efficiency gain; it represents a complete restructuring of how value is created.

For investors, that shift creates a timing problem. As AI compresses development cycles and accelerates go-to-market, value creation is happening earlier—often before most funds even begin to look. By the time capital arrives at Seed or Series A, much of the upside has already been realized, and the “AI premium” is priced in. The smart money isn’t asking whether to invest in AI, but when in the company’s life cycle to enter. The answer is: at formation stage.

The Formation-Stage Advantage

The AI efficiency gain creates a compelling opportunity for early-stage investors, but only if they can access companies before the AI valuation premium gets priced in.

AI startups command significant valuation premiums at every stage (PitchBook, Aurelia Ventures):

Seed: +42% over non-AI companies

Series A: +30% premium

Series B: +50% premium

AI SaaS companies trade at 29.7x revenue multiples compared to 6.6x for traditional SaaS (Aventis Advisors). These premiums mean that investors entering at traditional stages are paying premium prices for premium assets.

The formation stage, before these premiums are established, offers a different entry point. Companies at formation typically carry much lower valuations regardless of their AI capabilities. Investors who enter here capture the full benefit of AI-driven efficiency without paying the AI premium.

This timing difference translates to ownership economics. Formation-stage investors can secure 3x more ownership per dollar invested compared to those entering at Seed or Series A rounds (Stackpoint internal analysis).

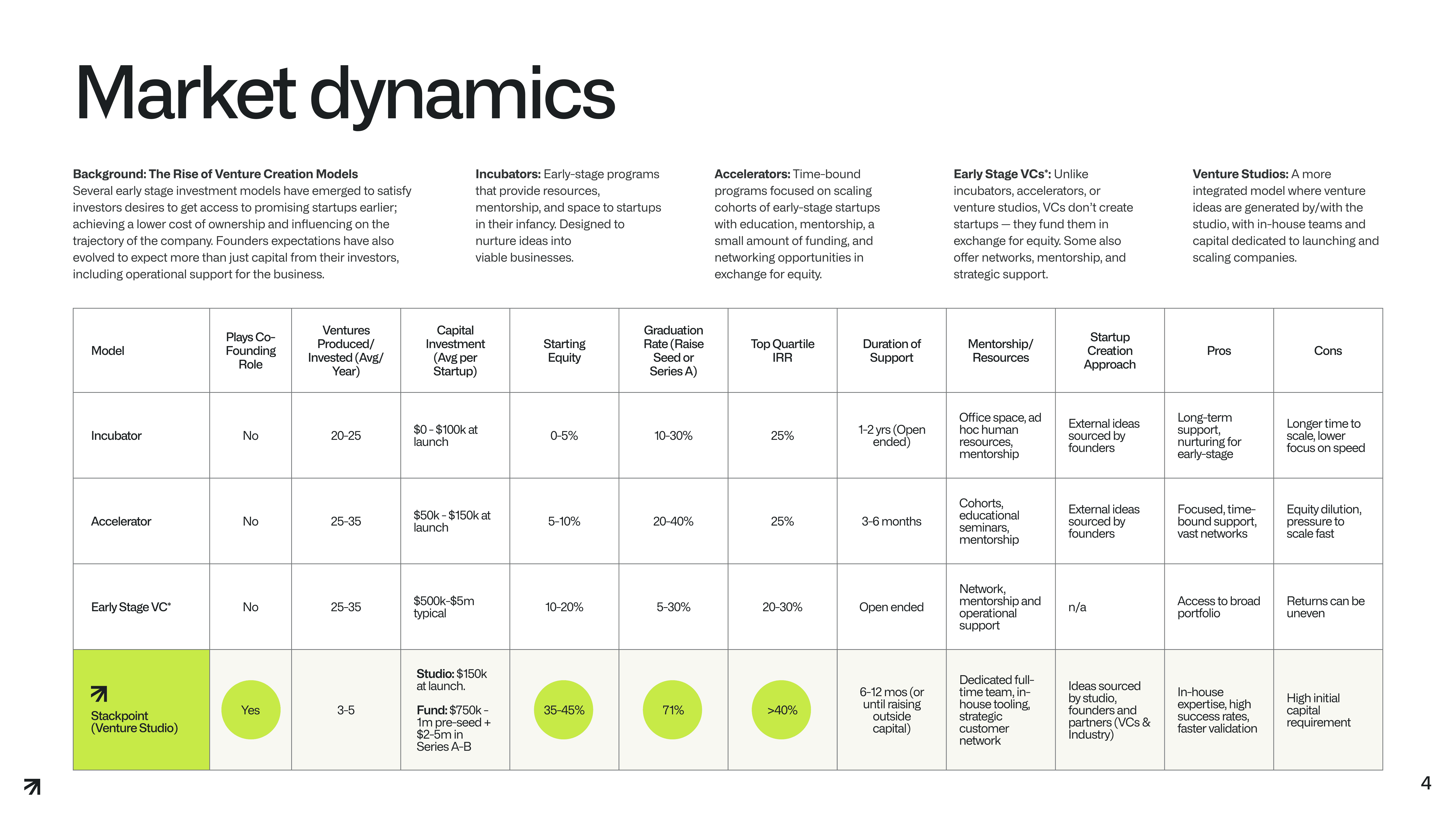

De-Risking Early Investment Through A New Model

One might argue that formation-stage investing could offer higher returns, but also carries higher risk. Most startups never make it to Series A, sometimes not because the ideas are bad, but because the execution chain breaks somewhere along the way. To succeed, a company needs more than a strong concept or a great founder—it needs the right early team, rapid validation cycles, early commercial traction, and the infrastructure to scale. Miss on any one of those, and the company stalls.

We founded Stackpoint Ventures to close that gap. As former founders ourselves, we knew firsthand all the challenges founders face in the early stage. Stackpoint’s venture studio model was built to solve that risk equation. Different from accelerators, incubators or VCs, Stackpoint co-founds the companies we invest in. Our full-stack studio integrates product, engineering, and go-to-market execution with dedicated funds and deep industry partnerships. This structure accelerates validation, compresses time to traction, and gives investors access to institutional-quality formation-stage opportunities—before valuations inflate and ownership dilutes.

We achieve this through three core pillars:

Full-Stack Execution Capability – Each company is built by an in-house team spanning product, design, engineering, go-to-market, and capital strategy. Our built-in recruiting function and deep talent networks help founders hire exceptional people fast—so they can focus on finding product market fit, not hiring or fundraising.

Validated Industry Opportunities – Every concept is shaped and tested through a proprietary discovery process with customers and industry insiders who often become early design partners, ensuring market demand from day one.

Capital and Network Leverage – Stackpoint deploys committed studio capital alongside a trusted network of VCs, design partners, and advisors in high-barrier industries such as real estate, finance, and insurance. This ecosystem accelerates customer acquisition and follow-on funding, resulting in a Seed-to-Series A graduation rate nearly 3× the industry average.

This model delivers formation-stage ownership economics with structured risk reduction—an institutional-grade approach to a historically high-risk, high-reward category.

The AI Execution Paradox

AI has made it faster and cheaper to build early prototypes—a small team can now spin up demos in weeks using off-the-shelf models and AI-assisted code tools. Yet while AI accelerates execution, it doesn’t replace the hard work of knowing what to build, who to build it for, and how to make it scale. Moving from prototype to production is a very different challenge that still requires deep market insight, disciplined iteration, and strategic execution.

Large-scale studies of over 150 million lines of AI-assisted code (LeadDev) reveal that while developers appear to move faster initially, they introduce higher levels of code duplication, rework, and fragility—often doubling the rate of code being rewritten or rolled back within weeks. Separate security audits found that AI-assisted developers produced less secure code while believing it was more secure.

In short: AI helps you draft faster, but it doesn’t replace the judgment, architecture, and engineering discipline required to build systems that stand up to real-world demands.

Vertical AI is about orchestrating data, compliance, reliability, and trust. Most low-code or “vibe-coding” tools were never designed for production systems handling private data, regulated workflows, or mission-critical processes. There is still no drag-and-drop platform today capable of delivering enterprise-grade AI with full observability, security, and governance.

That’s the gap Stackpoint addresses. We combine the speed of modern AI tooling with deep engineering rigor, industry-specific architectures, and co-development alongside design partners who operate in complex verticals.

We’re not waiting for someone else to build the “enterprise-ready” AI platform—we’re already building the systems those platforms will try to emulate.

Our advantage isn’t just moving fast; it’s knowing where to move fast. Stackpoint companies are engineered for the realities of regulated industries from day one, allowing them to scale securely and predictably—turning early efficiency into lasting enterprise value.

The winners in vertical AI won’t be those who ship faster. They’ll be those who ship correctly at scale.

Agentic AI Is the New SaaS

While coding assistant tools like Cursor and Lovable have posted rapid ARR gains, analysis of usage-based GenAI applications shows revenue can be volatile (spiking or dropping with little warning), and subscription retention/renewals have weakened industry-wide—conditions that can flatten growth after early surges. (L.E.K. Consulting, SubscriptionInsider).

The next generation of winners will look very different. Durable value will come from agentic AI—vertical, workflow-embedded systems that drive real business outcomes. These companies integrate tools, data, and decision logic into cohesive systems of execution that rewire how enterprises operate, leading to higher retention and sustained growth.

As Menlo Ventures notes, the defining trait of the next great software companies won’t be their interface or their access to the best models, but their ability to build adaptive, outcome-driven systems of work. In this “middle layer” of execution—where context, reasoning, and automation converge—AI becomes both useful and defensible.

In traditional software, middleware simply moved data from input to output. In AI-native systems, that layer now decides: what context to apply, which tools to invoke, and when to act versus observe. These agentic systems don’t just process information—they perform work.

This shift makes workflow-deep, domain-specific AI far more defensible than horizontal utilities. Instead of competing on access to foundation models, vertical AI companies win on data, process integration, and outcome ownership—the hardest advantages for incumbents to replicate.

Stackpoint focuses exclusively on building these vertical agentic AI companies in complex, high-barrier industries such as real estate, construction, finance, and insurance. These markets have well-defined workflows, abundant structured data, and measurable ROI from automation—conditions where agentic AI compounds value fastest. As Bessemer observes, the “built world” is a vast opportunity for vertical AI precisely because these sectors lag digitization yet yield high leverage when optimized.

Real-World Examples from Stackpoint’s Portfolio:

SurfaceAI built an autonomous Lease Audit AI Agent that continuously scans lease data, flags anomalies in real time, and routes them for resolution—turning what was once periodic manual review into always-on revenue protection. It operates as a digital employee, improving accuracy and eliminating revenue leakage.

LoanLight reimagines non-QM mortgage underwriting by dynamically matching borrower data to evolving investor guidelines. Its modular, model-flexible infrastructure supports multiple lending verticals and updates as better foundation models emerge—illustrating the power of adaptable systems of work built around AI’s strengths.

Both companies exemplify how Stackpoint’s approach converts AI capabilities into workflow ownership. They aren’t thin wrappers on foundation models; they’re autonomous systems that understand context, act on it, and deliver measurable business outcomes.

Where to Invest in the AI Value Chain

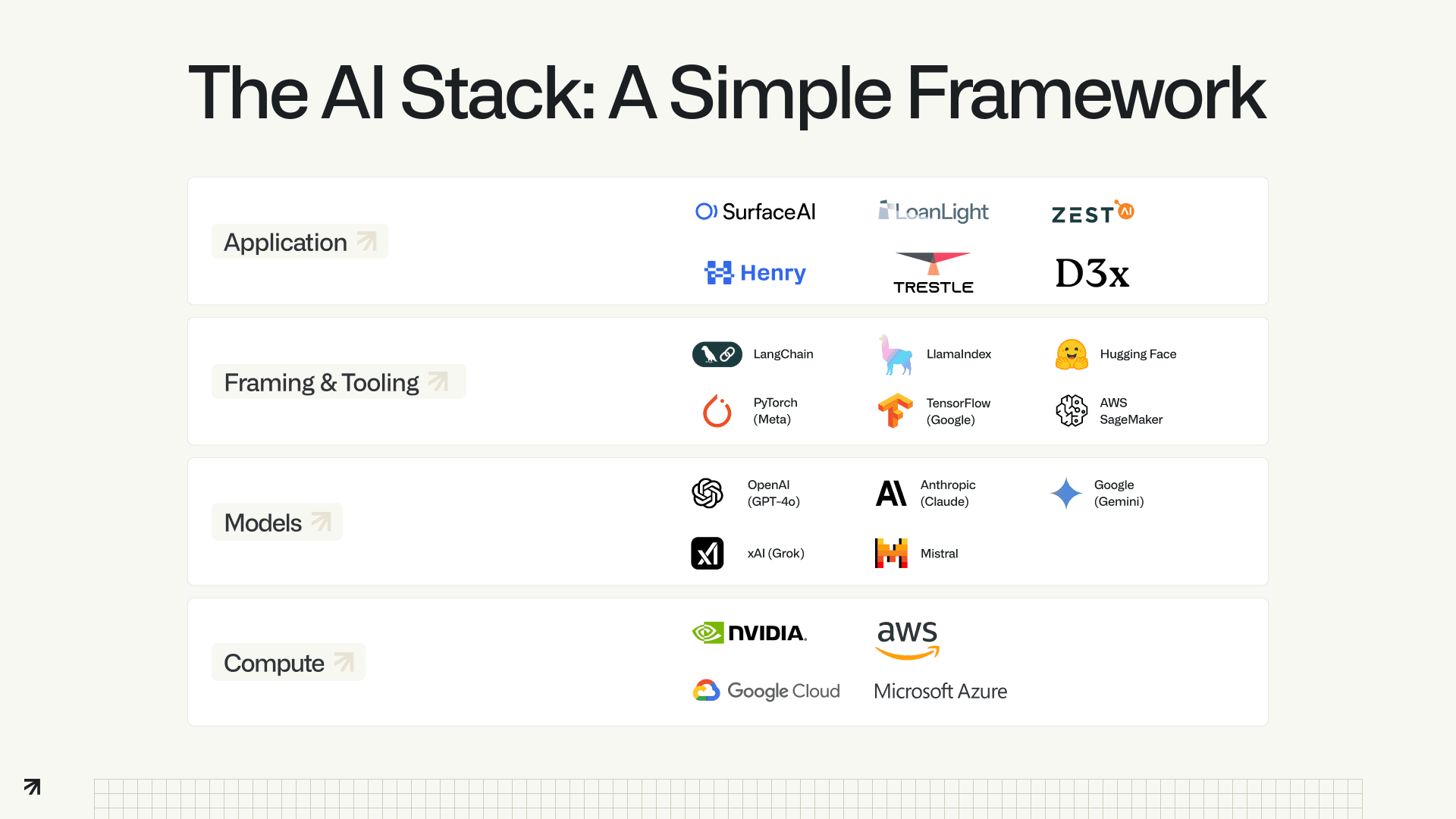

Investing in AI isn’t just about predicting which models will win—it’s about understanding where value accumulates in the stack. As detailed in Stackpoint’s recent white paper, Real Estate AI: A CEO’s Guide to What Matters Now, the modern AI ecosystem can be viewed through four layers:

Compute: the hardware and cloud infrastructure (Nvidia, AWS, Azure) that power model training and inference.

Models: the large foundation models such as GPT-4, Claude, Gemini, and Mistral, which interpret language, vision, and logic.

Frameworks & Tooling: developer infrastructure like LangChain, LlamaIndex, and TensorFlow that connect models to data and workflows.

Applications: the software layer where real users interact with AI through purpose-built tools that integrate into business processes.

While much of the early investment attention has flowed toward the model and compute layers, those markets are already dominated by a few hyper-scale players and capital-intensive bets. For most investors, that means the most defensible and scalable opportunities now sit higher up the stack—in the application layer, where AI delivers measurable workflow transformation in mature industries.

This is where vertical AI and agentic AI systems create true enterprise value. Application-layer companies build on top of commoditized models and infrastructure, focusing instead on data quality, domain context, and deep integration into existing work. These systems don’t just provide insights—they execute work autonomously within industry-specific workflows, producing repeatable ROI such as the examples above from SurfaceAI and Loanlight.

These application-layer businesses demonstrate why vertical AI represents the most attractive point of entry for investors. The products are closer to revenue, their value is easier to quantify, and their defensibility stems from proprietary workflows and relationships rather than model performance alone.

In other words, the winners in the next phase of AI will be the companies embedding AI into real work, turning automation into competitive advantage, and predictable workflows into scalable enterprise systems.

Conclusion: What This Means for Investors

AI has restructured startup economics, enabling lean teams to achieve scale with minimal capital. Value creation is concentrating in vertical, workflow-deep, agentic systems. And capturing that value requires professional execution at the formation stage, before the AI premium sets in.

Stackpoint’s full-stack venture studio is built for this new environment. It gives investors early access to high-barrier opportunities, professionalized execution to de-risk outcomes, and exposure to the class of AI companies most likely to generate lasting enterprise value.

For investors, the question is no longer whether to invest in AI, but when and where. Those who engage earlier, through structured formation partnerships and a focus on vertical, agentic AI, will capture the most valuable equity—right when risk is lowest and upside greatest.